Payment Hub vs. Legacy FT: What Banks need to know before it’s too late

March 11, 2026

Banks across ASEAN, Pakistan, and the MEA region face an urgent imperative i.e., to modernize payments before regulatory deadlines and customer expectations outpace them. Global mandates like SWIFT’s ISO 20022 migration for cross-border payments (CBPR+) are already close to the final deadline of implementation, while regional systems are moving even faster, such as China’s RMB clearing via CIPS and Saudi Arabia’s SARIE RTGS, which became ISO 20022-compliant in 2023.

However, with legacy systems, cross-border payments have been a daunting challenge for businesses and consumers alike. Sending money through legacy systems often involve complicated procedures, lengthy delays, and high transaction fees. Legacy payment systems, built on outdated infrastructures, struggle to handle the complexities of global transactions, often requiring intermediaries and multiple steps to complete a simple transfer. These systems are rigid, inefficient, and lack the flexibility to meet the growing demands of a fast-paced, interconnected world.

With limited access to real-time payment solutions and no unified platform for diverse payment methods, the process becomes a bottleneck for international trade and personal transactions. As the world moves towards online cross-border payments, the need for faster, cheaper, and more secure payment systems become undeniable. This sparks the development of payment methods, mandates and hubs that are scalable, flexible and interoperable.

Analyzing the need to adapt to modern payment hubs

As customers demand instant payments, real-time transaction tracking, and global accessibility, banks are under increasing pressure to provide these services. Payment solutions that support the requirements of the current era don’t just allow enterprises and consumers to accept payments; instead, they empower them to thrive in the complexities of the digital economy.

Innovative payment hubs today allow banks to address the shortcomings of legacy systems and provide seamless, real-time solutions for cross-border payments, ushering a new era of financial transactions. A well-designed payment hub enables banks and other financial institutions to process payments through a central platform, whilst ensuring compliance with regional rules and regulations. Payment hubs further allow banks to modernize their existing components as the new mandates are introduced, to remain competitive in the digital payment landscape.

Failure to embrace modern payment hubs can have severe consequences for banks. By continuing to rely on legacy systems, banks risk falling behind competitors who have already adopted advanced solutions, leaving them unable to meet the demands of a digital-first world. Since customers expect instant, frictionless experiences, banks that fail to provide experience a serious decline in customer satisfaction and loyalty.

Legacy systems, due to their limitations, are costly to maintain, and are more prone to errors leaving them vulnerable to security breaches. This ultimately increases the risk of fraud and compliance issues. Banks that do not adapt to updated payment systems may also struggle to comply with evolving regulatory requirements, risking fines and reputational damage.

In an era where agility and innovation are paramount, failing to modernize payment infrastructure could result in losing market share, diminishing profitability, and ultimately, becoming irrelevant in the financial services industry.

Why legacy funds transfer methods are no longer applicable

Legacy Funds Transfer modules are generally built for older MT messages and batch processing simply cannot keep up. They lack real-time ISO 20022 capabilities, are inflexible, and impose heavy compliance and operational risks.

By contrast, a modern payments hub like Temenos Payment Hub is designed to meet these challenges head-on. It natively handles ISO 20022 and real-time schemes, scales horizontally (cloud or SaaS), and offers API-driven integration with digital channels. Banks that cling to FT risk falling behind in compliance, customer experience, and cost efficiency.

The legacy funds transfer problem

Traditional FT modules are effectively “end-of-life” payment engines with no roadmap for new features. They suffer from multiple critical pain points:

- Outdated functionality: FT systems cannot process instant or 24/7 payments and offer limited payment schemes.

- Poor flexibility: Legacy FT is typically monolithic and on-premises. It cannot flexibly scale to higher volumes or integrate easily with cloud and API platforms.

- Compliance and tech debt: Built around MT formats, FT cannot natively handle new regulatory standards such as SWIFT CBPR+, SEPA 2023, and local rulebooks.

- Market shortcomings: Without real-time rails or rich data, banks using FT struggle to meet digital customer expectations. They can’t easily offer instant payments.

- High cost and operational risk: Manual processing and exceptions are common in legacy systems; payments are not truly straight through. Fraud controls and real-time response to cyber threats are limited, and maintenance costs skyrocket as the codebase ages.

The inability to process new payment types or meet 24×7 fraud-screening requirements leaves institutions vulnerable to errors, delays, and regulatory fines. Legacy FT undermines straight through processing, raises the total cost of ownership, and prevents banks from capitalizing on modern payment opportunities.

Why leading global banks embrace modern payment hub

Given the complexities of the ever-evolving payment landscape, next-generation payment hubs are explicitly designed to overcome all the shortcomings of the legacy systems. It consolidates every payment type and process logic into one platform.

Unlike FT, modern payment hubs support all payment types (instant credit transfers, traditional credit transfers, debits, cheques, bulk files) and all schemes, including SWIFT, domestic RTGS, QR/instant, and request-to-pay. Temenos Payment Hub is one such example, that is widely accepted and implemented across various banks, and covers capabilities of a modern payment system. Some of its key features include:

- Built for real-time 24/7 processing and has an API-centric design. It integrates seamlessly with online and mobile channels and fintech ecosystems, which enables instant credit transfers and real-time confirmations for customers.

- Uses a universal processing flow that maximizes straight-through rates. Features like payment warehousing and routing logic are built-in, whereas FT would require expensive customizations.

- The hub is multi-tenant, cloud-ready and customizable. It can run as SaaS, in the cloud, or on-premises, either embedded within Temenos Transact or alongside any core system. This flexibility lets banks scale quickly and cost-effectively.

- TPH supports SWIFT GPI tracking, SEPA instant credit, request-to-pay, and other innovations without heavy redevelopment. It positions banks for a cashless, real-time payments environment that meets evolving customer expectations.

Compliance to regulations and regional mandates

Banks in ASEAN, Pakistan, and MEA are juggling multiple compliance requirements simultaneously. SWIFT’s 2025 ISO 20022 mandate for cross-border payments is the most pressing global deadline. At the same time, regional systems like CIPS in China and SARIE in Saudi Arabia are enforcing ISO 20022 adoption, and the UAE’s major platforms are scheduled for migration by 2025. Banks that fail to upgrade risk being disconnected from these ecosystems.

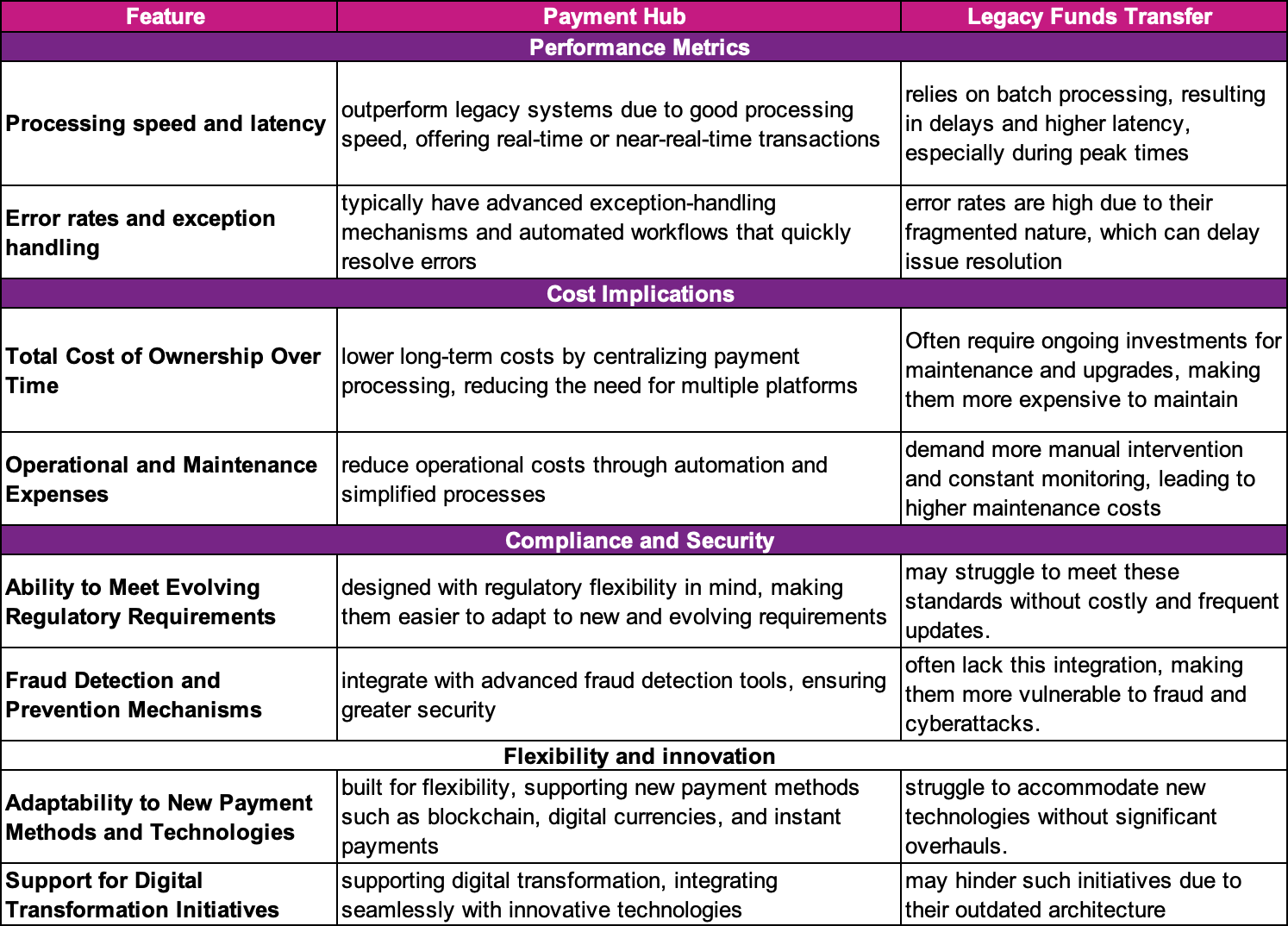

Comparative Analysis: Payment Hub vs. Legacy FT

Future-ready: open banking and beyond

Banks in ASEAN, Pakistan, and MEA are juggling multiple compliance requirements simultaneously. SWIFT’s 2025 ISO 20022 mandate for cross-border payments is the most pressing global deadline. At the same time, regional systems like CIPS in China and SARIE in Saudi Arabia are enforcing ISO 20022 adoption, and the UAE’s major platforms are scheduled for migration by 2025. Banks that fail to upgrade risk being disconnected from these ecosystems.

Integrating a modern payment hub like TPH lays the foundation for open banking and next-gen innovation. Its API-first design supports PSD2 use cases, while ISO 20022 data unlocks AI-driven fraud detection and analytics. Banks can quickly add features like QR-based payments or blockchain-based settlement thanks to TPH’s modular architecture.

Act now or be left behind

By November 2025, SWIFT MT messages will be obsolete, and ISO 20022 will be the global norm. Regional systems like SARIE and CIPS are already live. Legacy FT modules cannot meet these demands, and delaying modernization will only increase costs and compliance risks.

Moving to Temenos Payment Hub ensures compliance, operational efficiency, and future-proof innovation. With Systems Limited’s proven expertise and accelerators, banks can achieve this transformation quickly and confidently.

The time to modernize is now. Contact us.

Quick Link

You may like

How can we help you?

Are you ready to push boundaries and explore new frontiers of innovation?